7 February 2022 – A recent Kaspersky research showed that e-payment adopters in Southeast Asia (SEA) are becoming increasingly aware of the importance of safeguarding their financial data amidst the rapid rise of digital payment use in the region. And they are clear on the additional security features they hope to see implemented by banks and mobile wallet providers here, moving forward.

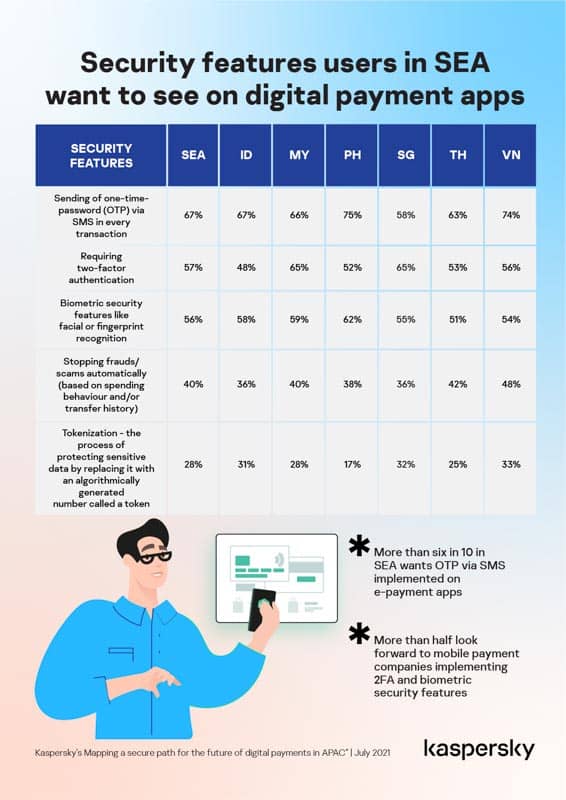

Titled “Mapping a secure path for the future of digital payments in APAC”, the study discovered that more than three in five (67%) users of digital banking and e-wallet apps in SEA prefer the implementation of one-time-passwords (OTPs) through SMS for every transaction.

Majority of the respondents also want to see the implementation of two-factor authentication or 2FA (57%) as well as biometric security features like facial or fingerprint recognition (56%).

Interestingly, the implementation of OTPs is the top priority for consumers in most SEA countries – including Indonesia (67%), Malaysia (66%), The Philippines (75%), Thailand (63%), and Vietnam (74%) – except Singapore where two-factor authentication is the most urgent concern (65%).

Digital payment customers also welcome the use of machine learning in combatting social engineering attacks. Almost half (40%) noted that companies should start preventing frauds/scams automatically based on spending behaviour and/or transfer history.

Over a quarter (28%) also said Tokenization – the process of protecting sensitive data by replacing it with an algorithmically generated number called a token – can also augment the security of mobile banking and e-payment applications in the region.

“SEA’s sheer market size in terms of digital payment offers a lengthy runway for expansion. In a competitive sector, payment companies should be assessed not just on their innovations, but also on their security posture. We can draw from our findings that customers are increasingly becoming aware of the value of technology to protect their finances online. In general, these security features are useful preventive measures that can potentially enhance the cybersecurity standards in the digital payments space. However, these options should not be viewed in an isolated manner, but considered as part of a holistic cybersecurity framework,” says Yeo Siang Tiong, General Manager for Southeast Asia at Kaspersky.

The usage of two-factor authentication, for example, has its limitations, particularly when it comes to SMS-based authentication.

Password-bearing SMS messages can be intercepted by a Trojan lying inside the smartphone, or by a defect in the SS7 protocol used to transmit the messages, making SMS-based 2FA unreliable at times. In such cases, it would be advisable to employ self-contained authenticator apps, with SMS being used only as a last resort to limit a company’s vulnerability to data breaches.

With the complicated nature of securing apps and finances online, it is not surprising that over three in five (65%) of the respondents said that banks and mobile wallet companies should provide more incentives to maintain the security decorum – such as changing passwords regularly. Another 60% noted that providers should educate users more about the threats online.

When it comes to choosing a mobile e-wallet provider, security remains a priority for digital payment users in SEA.

More than half (58%) said they will use an e-wallet that includes extra security features like fingerprint and 2FA while more than a third (37%) said they will use banking apps or mobile wallets from providers that have not have been engaged in any previous data breach or cybersecurity attack.

A number of respondents also noted that mobile e-wallet has to be independent – can be used directly by a bank or through a third party (42%) or a closed one – linked to specific merchants, where users can only use the funds to make payments for transactions initiated with the specific merchant (35%).

Another set of considerations in choosing a digital wallet company includes apps should offer promos, cashback, lower transfer fees (49%); provide anonymity – users don’t need to reveal credit card details to too many merchants (35%); be bankless – bank account details not needed (25%); and be locally made (16%).

“To develop a long-term and sustainable growth strategy, digital payment companies need to take into account some of the wants and needs of their users. While some of the preventive measures are not entirely new and have been around for some time, it is crucial to consider how security features can be integrated in a manner without compromising the user experience. Our study showed how customers are increasingly holding digital payment providers accountable to the security of their finances online so we suggest companies to determine the cybersecurity gaps in each of the stage of their payment process, and fit in the right IT measures in a calibrated manner,” adds Yeo.

To stay protected from ever-changing fraud and cybercrime techniques, Kaspersky recommends digital payment providers to adopt the following measures:

To read the full report, please visit https://kas.pr/b6w8.